Unpacking the Department of Energy’s Report on US Liquefied Natural Gas Exports

This paper examines the Department of Energy's report, alongside analysis from S&P Global, revealing that the department likely underestimates methane emissions and the rising prices driven by increased US LNG exports.

1. Introduction

Long one of the world’s largest natural gas producers, the United States has now leaned into exporting the fuel overseas in the form of liquefied natural gas, or LNG. US LNG exports rose from less than 0.1 billion cubic feet per day (Bcf/d) in 2015 to nearly 12 Bcf/d in 2023. The United States has now surpassed Australia and Qatar as the world’s largest LNG exporter.

Following a year-long pause in approvals of new LNG export permits, in December 2024 the Department of Energy (DOE) published “Energy, Economic, and Environmental Assessment of U.S. LNG Exports” (DOE 2024), a report assessing the consequences of continued increases in US LNG exports out to 2050. On January 21, 2025, the newly inaugurated Trump administration lifted the permitting pause and extended the window for submitting public comment on the report through March 20. This still-live report estimates how an expansion of US LNG exports would affect domestic energy prices and global greenhouse gas (GHG) emissions, along with many other economic and societal outcomes. Other views on the matter include an analysis by S&P Global (Yergin et al. 2024).

The complex modeling needed to make predictions necessarily requires many assumptions, some of which are subject to critique and debate. Rather than taking on the entire DOE report, we focus on four aspects of the modeling effort: (i) methane emissions that leak from the gas supply chain, (ii) impacts on US natural gas prices, (iii) projections of the highly uncertain future global demand for US LNG, and (iv) how energy consumers may substitute between LNG imports and other energy sources. Where appropriate, we also compare our findings with the S&P Global report.

2. Methane Emissions from the US Supply Chain

A big issue in the debate over LNG exports is the role they may play in exacerbating or mitigating climate change: while LNG emits less CO2 than coal when burned, the oil and gas infrastructure that produces LNG emits methane, a highly potent GHG. A recently published and frequently cited study by Robert Howarth (2024) made the startling assertion that exported US LNG is more carbon intensive than coal. Whereas that study assumed a 2.8 percent rate of methane leakage during the upstream and midstream stages of gas production (extraction and transport to liquefaction facilities), the DOE report assumes a much lower rate, 0.56 percent. DOE’s value comes from a report by the National Energy Technology Laboratory that was released contemporaneously with its LNG exports report (DOE 2024) and is meant to reflect a US average, based largely on estimates from the Environmental Protection Agency’s Greenhouse Gas Reporting Program and Greenhouse Gas Inventory, both of which rely primarily on engineering models rather than direct in situ measurements. Yet the scientific empirical literature using remote sensing techniques has repeatedly found methane leak rates several times larger than those estimates (e.g., see Alvarez et al. 2018; Omara et al. 2018; Zhang et al. 2020; Chen et al. 2022; Omara et al. 2022; Lu et al. 2023; Sherwin et al. 2024).

For example, Sherwin et al. (2024) used 1 million aerial (aircraft and satellite) site measurements for six major oil and gas-producing US regions. They found widely ranging methane leak rates across locations, from a low of 0.75 percent in parts of Pennsylvania to a high of 9.63 percent in the New Mexico Permian basin, with a six-basin average of 2.95 percent. Thus, DOE’s assumed value of 0.56 percent is 25 percent smaller than even Sherwin et al.’s lowest one and about one-fifth of the six-region average of 2.95 percent.

The DOE value also comes out as a fifth of the 2.8 percent estimate used in the Howarth (2024) paper, which took the estimated 5.3 percent average leak rate in the Permian basin from Sherwin et al. (2024) and carved out a share attributed to gas rather than oil. The logic behind focusing on the Permian basin is its relative proximity to the Gulf Coast, the location of most existing US LNG export terminals.

But in both cases, the underlying assumptions do not reflect the economics of the situation. First, even if the physical molecules could be tracked from the Permian basin to LNG terminals (which is an infeasible task on a pipeline network), the economic scarcity created by the additional LNG demand will spur more production from the most price-responsive supplier—not necessarily the closest one or the one contracted. Second, what matters for the climate is the total methane emissions caused by an increase in gas exports, not merely the share of those emissions “attributed” to gas in some manner. If gas demand induces 100 units of gas production that leaks at a rate of 5.3 percent, the fact that another 100 units of oil production come along for the ride doesn’t mitigate the emissions from the gas in any meaningful way—if anything, the additional oil production will drive further emissions.

Therefore, both the 0.56 percent and the 2.8 percent methane leak rate values are inappropriate, but for different reasons. The appropriate value would take into account the economics of oil and gas markets and reflect the marginal source of gas supply that rises to meet increased LNG export demand. The Permian basin is primarily an oil play, and the “associated” gas that comes out of the ground with the oil is not the main reason operators drill those wells. An RFF working paper by one of this issue brief’s coauthors (Prest, forthcoming) finds that gas export demand is likely to be met primarily by low-leak Appalachian supply (followed by the Haynesville shale), but very little of it will likely be met by higher gas production in the high-leak, oil-focused Permian basin. The central result is that the marginal gas supply that ramps up to meet export demand has an effective methane leak rate of about 1.7 percent, about halfway between DOE’s 0.56 percent and Howarth’s 2.8 percent. In other words, accounting for empirical evidence on methane emissions and the economics of gas markets would triple DOE’s assumed leak rate while reducing Howarth’s by more than a third. This would have substantial implications for both studies’ findings, although in opposite directions.

3. Effects on US Natural Gas Prices

The DOE study also assesses the effect of exporting LNG on US natural gas prices, estimating that a 32.6 Bcf/d increase in LNG exports—which is about 30 percent of US gas supply—will raise US wholesale gas prices at Henry Hub from $3.53 to $4.62/MMBtu (DOE 2024, S-27), a 31 percent increase. This comes out to a 0.95 percent price increase per Bcf/d of exports. But the results in the RFF working paper (Prest, forthcoming) suggest an increase of about 2.5 percent per Bcf/d of exports, more than twice the size of DOE’s estimate. That is, domestic gas prices could rise substantially more than DOE anticipates (and even more than the S&P Global study suggests), lessening consumption and thereby reducing CO2 emissions from combustion.

Why is DOE’s estimate so small? It appears that DOE’s model used a very large implicit elasticity of gas supply of about 1, which implies that each 1 percent increase in gas demand is associated with a 1 percent increase in price—a very flat supply curve for a commodity that is traditionally considered inelastically supplied. That supply elasticity is far higher than what RFF and other researchers have found. Indeed, Prest (forthcoming) estimates a long-run gas supply elasticity of less than 0.3, or less than a third of what DOE’s model implies. This, coupled with a reasonable assumption for the elasticity of gas demand of about –0.2, suggests a price increase more than twice DOE’s.

4. Future Global Natural Gas Demand and US LNG Exports

The need for and success of LNG export growth also depends on the potential market for it. The complex modeling process to estimate the size of the market usually starts with a prediction of global energy demand, proceeds to estimate the share of global demand met by natural gas, and from there anticipates the global demand for LNG and for US LNG in particular.

Predicting global energy demand has become something of an industry. It is very difficult to predict future natural gas demand because the fuel is used in multiple sectors, from electricity generation and industrial plants to household heating, and often fills gaps in the availability of other fuels. Further, future gas demand will depend on the success and spread of carbon capture and sequestration (CCS) technology.

Predicting demand for LNG—and, from there, US LNG exports—requires looking at all the major sources of supply and assessing their availability and price by region. Both supply and demand depend on policy assumptions, technological and socioeconomic forecasts, and both natural gas prices (whether produced from local sources, transmitted by pipeline, or shipped after liquefaction) and the price of substitutes. And prices, of course, are determined by the interplay of supply and demand.

The DOE report follows those steps and deals with the uncertainty of future demand by modeling 20 scenarios, many of which assume that national CO2 commitments pledged in Paris are met. Some are even more optimistic and assume that net-zero CO2 emissions are achieved by 2050. The report also includes a business-as-usual (BAU) scenario termed “Defined Policies: Model Resolved,” which takes the Inflation Reduction Act, Infrastructure Investment and Jobs Act, and other existing US and rest-of-world (ROW) policies into account but assumes no future policy initiatives. Irrespective of the near-term US situation, the future global outcome is likely to fall somewhere between the BAU and net-zero extremes. Predicting the relative likelihood of DOE’s scenarios is unrealistic, as the agency acknowledges. Figure 1 is reproduced from the report, showing results for the five base-case scenarios. It also indicates levels of existing capacity plus FID (final investment decision) capacity and approved export capacity, none of which were affected by the 2024 pause. This estimate mirrors the pattern for global LNG demand: a relatively slow increase through 2030 that ramps up more rapidly through 2040 and beyond (Table 1).

Figure 1. DOE Projections of US LNG Exports, by Scenario

Source: Department of Energy, with graphics by OnLocation.

The main finding is that DOE-approved LNG export capacity is large enough (43.6 Bcf/d) to meet demand in all but the BAU scenario. And even in that case, demand is more than met through 2040. Another important result is that demand for US LNG exports is relatively flat until 2030, at which point it ramps up in all but one of the scenarios shown.

Those estimates can be usefully compared with the S&P Global results (Yergin et al. 2024), released the same day as the DOE report. In S&P Global’s base case (Figure 2), global LNG demand increases 64 percent, from about 48 Bcf/d (365 MMt) in 2020 to about 81 Bcf/d (600 MMt) in 2030, flattening thereafter through 2040. US LNG exports follow a fairly similar pattern but increase 270 percent, from about 6 Bcf/d (47 MMt) in 2020 to about 24 Bcf/d (174 MMt) by 2030, beyond which they are basically flat.

Figure 2. S&P Projections of Global LNG Supply

Source: S&P Global. MMT = million metric tons.

The supply of US gas exports (assuming no permitting pause) is higher in 2030 in the S&P Global analysis than in DOE’s, suggesting that a continued pause would tighten the global market in the near term. The S&P projection of 24 Bcf/d for 2030 is very close to what DOE has approved and is ready to be built (FID). Because it takes a few years to build an LNG plant and get it operating and fully permitted, the implication is that any further permitting delays could leave money on the table. The DOE estimate, by contrast, is far below FID through 2030, suggesting plenty of headroom to meet demand as estimated by their analysis. In 2040, however, the situation looks much different: DOE forecasts a big increase in US LNG supply (if still under the approved cap), whereas S&P Global suggests that the US role will be virtually unchanged from 2030.

Table 1 summarizes the above categories of natural gas demand for the DOE study, the S&P Global study, and projections from the International Energy Agency (IEA), which can be assumed to be more neutral in its stance on LNG permitting. Estimates have been converted to the same units as in the DOE study (Bcf/d). IEA is more conservative in its estimates for global LNG demand than either DOE or S&P Global.

Table 1. Gas Demand and Supply Projections from the Department of Energy (DOE), S&P Global, and International Energy Agency (IEA)

Note: All units in billion cubic feet per day (Bcf/d) (conversion: 1 MMt = 48.7 Bcf, or 0.133 Bcf/d).

Sources: Department of Energy (DOE), S&P Global, International Energy Agency (IEA), and authors’ calculations.

5. What Do US LNG Exports Replace?

How lifting the pause will affect global CO2 emissions, co-pollutants, and energy markets depends heavily on the energy sources for which US LNG substitutes—a complex question that requires detailed modeling and many assumptions.

Conceptually, given the price of imported LNG and a country’s gas distribution network, the effects could follow several pathways. The first is that putting additional US gas supply on the global market substitutes in part for gas from other countries. Whether this would increase or decrease GHG emissions depends on the relative emissions footprint of the US LNG export supply chain versus that of the countries whose gas is being displaced. Substituting US LNG for gas from Russia or Algeria, for instance, could reduce GHGs if these countries have a higher methane leak rate, so long as the added emissions from liquefaction, shipping, and re-gasification are small relative to those of pipeline transport from these countries to users. Gas from Qatar, on the other hand, is generally viewed as “clean.”

But the added global supply from additional US exports could well lower global gas prices, and that alone could lead to greater use of natural gas in new energy services—generating electricity, heating homes, and fueling industry—that would not otherwise have happened. These increases in gas consumption would not be offset by reductions elsewhere, so they translate directly into an increase in total GHG emissions.

The third possibility is that the new US gas substitutes for other fuels. In this case, the effects on GHG emissions depend on the carbon footprint of the US LNG exports and the footprint in the importing country, compared with the footprint of the fuel being replaced. The GCAM model used in DOE’s study recognizes five substitution possibilities: coal, oil, renewables, other sources including nuclear power, and fossil fuels with CCS.

Carbon footprints across countries and fuels vary tremendously. Even within the United States, there is significant heterogeneity across gas and oil (with associated gas) plays, further complicated by factors such as disagreement about methane leak rates across estimation methods, as discussed above. To take one example, the influential and controversial paper by Robert Howarth (2024) (a previous version of which was critiqued in a blog post by Jonah Messinger of The Breakthrough Institute) suggests that the US LNG footprint is 33 percent more carbon intensive than coal—a departure from conventional wisdom, to say the least. The DOE report, by contrast, does not adopt this position or the assumptions that led to Howarth’s conclusion. Further, the emissions intensity of energy systems in countries importing LNG can vary widely. For example, newer or better-maintained pipelines may minimize leaks, and CCS technology on gas-fired boilers or turbines can reduce emissions tied to combustion.

The DOE analysis of those pathways is displayed in Figure 3, which shows the 2020 to 2050 cumulative increase in US LNG exports (113 EJ, which represents the cumulative energy content of LNG exports from 2020 to 2050). Interestingly, the analysis finds that a substantial degree of US LNG exports (37 percent) displace ROW gas production. Of the remaining 63 percent that adds to global gas consumption, only a small fraction (4 percentage points) uses CCS. Ultimately, increased total energy use accounts for 13 percent of total US LNG exports. Another 13 percent substitutes for coal, 6 percent for oil, and unfortunately, based on the economics of zero-carbon energy (including nuclear energy) versus US LNG, more than 25 percent of the gas substitutes for these zero-emission sources. In all, the analysis predicts a cumulative increase of about 710 MMT of CO2-equivalent (CO2e) emissions between 2020 and 2050. The implication is clear: business as usual is bad for the climate. Note, however, that this increase represents only about 0.05 percent of predicted cumulative global CO2e emissions (see Table ES-2 of the Executive Summary of the DOE report).

Figure 3. DOE Assessment of What US LNG Exports Substitute For

Source: Department of Energy, with graphics by OnLocation.

Note: Zero/low carbon-to-gas substitutions include displacements of renewables (dark green), nuclear (medium green), and other fossil CCS (light green). Unabated fossil-to-gas substitutions include displacements of coal (orange) and oil (brown). CCS = carbon capture and sequestration. EJ = exajoule (10^18 joules). ROW = rest of world.

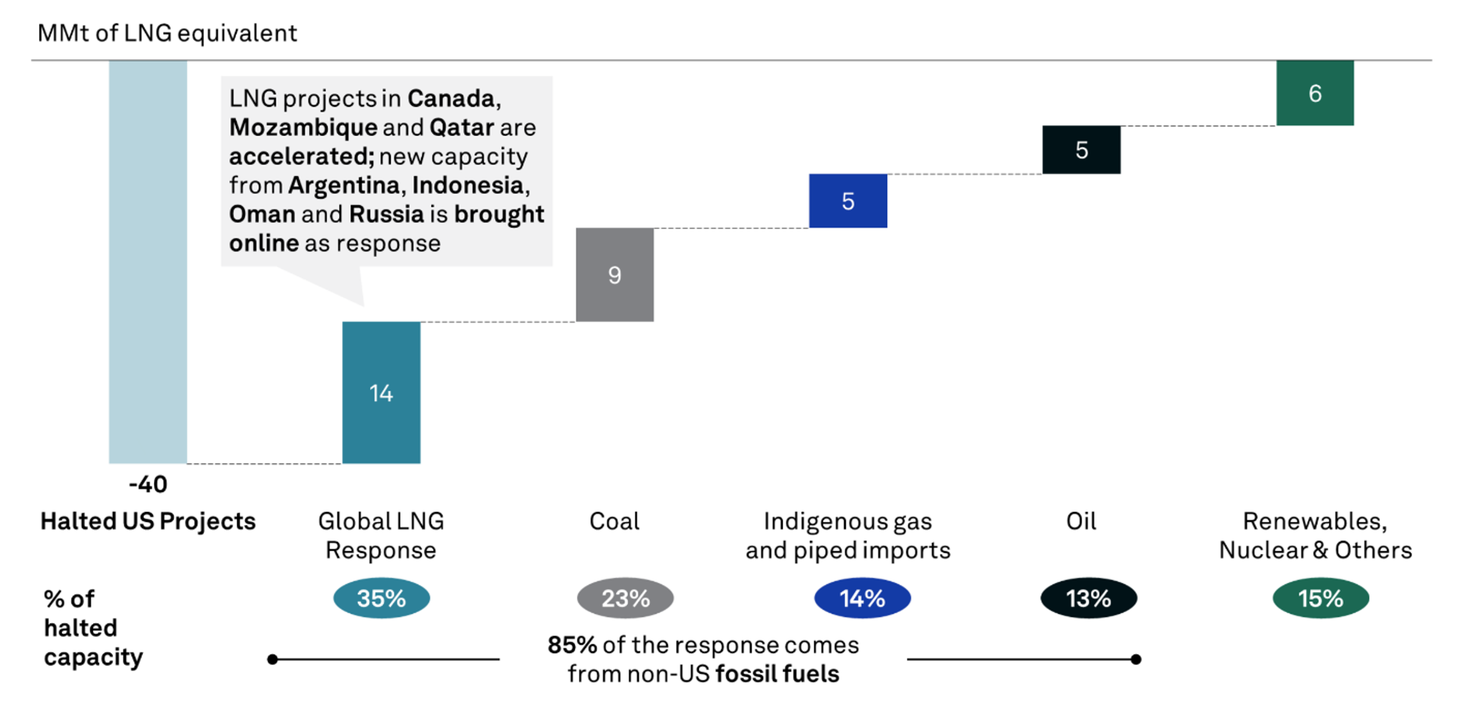

We now return to the S&P Global (2024) analysis for another perspective on what will happen in the rest of the world in response to a big increase in US LNG exports (Figure 4). In contrast to the DOE analysis, the time frame is shorter and starts later (2028 to 2040 vs. 2020 to 2050). Also, from an expositional perspective, the scenarios are reversed to be the consequences of a “halt” in LNG permitting rather than the consequences of expanded export capacity. In the discussion below, we take the DOE perspective of expanded exports.

Figure 4. S&P Assessment of What US LNG Exports Substitute For

Source: S&P Global.

S&P Global similarly estimates that US LNG would displace a mix of energy sources but a more carbon-intensive one than DOE estimates. Table 2 includes a side-by-side comparison of the DOE and S&P substitution patterns. In S&P’s analysis, 35 percent of the added US LNG production displaces new planned LNG projects in ROW and another 14 percent reduces other gas production (local gas and gas shipped by pipeline). Together, this is almost 50 percent of the added US LNG exports replacing ROW gas production. In contrast, DOE finds that only 37 percent of US LNG production displaces ROW sources and that 13 percent spurs additional energy consumption. We could not find a comparable estimate for this rebound effect in the S&P Global analysis. Its absence means that S&P Global does not appear to be accounting for the GHG increase associated with the higher energy demand induced by lifting the halt via lower ROW natural gas prices. S&P Global also finds that more of the LNG displaces coal (23 vs. 13 percent) and oil (13 vs. 6 percent) but less displaces non-fossil energy (renewables plus nuclear and others, 15 vs. 25 percent). Assuming that the US LNG CO2e footprint is cleaner than elsewhere, this analysis—with larger cutbacks in ROW natural gas, coal, and oil, and smaller cutbacks in renewables and nuclear—is much more favorable to expanding gas exports than DOE’s. The effects of all this on net GHG emissions, while directionally clear, are expected to be the subject of a forthcoming second report from S&P Global in March 2025.

Table 2. LNG Substitution Patterns, Department of Energy (DOE), and S&P Global

Sources: Department of Energy, S&P Global, authors’ calculations.

Note: ROW = rest of world.

It is worth noting that the United States is such a large consumer of natural gas that what happens to domestic emissions here can significantly affect global carbon emissions. Higher US natural gas prices from expanding LNG exports will reduce US natural gas consumption, including in the power sector. And with coal on the way out in the electricity sector, the gap will likely be met by lower-carbon sources like renewables and possibly nuclear. Thus, the price-induced reduction in US gas consumption will likely reduce domestic CO2 emissions, although as previously noted, US methane emissions would rise from higher gas supply. As home heating and vehicles are increasingly electrified and as industry turns away from direct use of natural gas, what happens in the electricity sector will become more important in assessing net emissions effects.

6. Packing It Back Up

So what does this all mean? First, DOE is likely underestimating the methane emissions and price increases that will be driven by increased US LNG exports. The effects in the United States push in opposite directions, however, with higher methane emissions in gas supply chains but lower CO2 emissions from reduced gas consumption. Second, substantial uncertainty about the long-run demand for LNG remains, driven by both economic factors and global environmental goals. Third, LNG will likely substitute for a mix of higher-carbon and lower-carbon energy sources, but it is not yet certain whether the effect on global emissions will be positive or negative. Altogether, these conclusions suggest that the impacts of DOE’s pause for the future US role in the global gas market—on both the cost and benefit sides of the ledger—have been overhyped in the public debate on the issue. It will take many years (until 2040 according to DOE and even longer according to S&P Global) before the demand for US LNG will exceed the amount of export capacity already approved. And to the extent that major Asian countries—the sources of much long-term demand in a business-as-usual case—adopt more aggressive policies to limit greenhouse gas emissions and move away from natural gas, the business case for not-yet-approved gas exports will look shakier still.

{kind=link}